The Achieving a Better Life Experience (ABLE) Act allows individuals with disabilities to establish tax-advantaged savings accounts, ABLE accounts, to cover qualified disability expenses. These accounts, similar to college savings accounts, enable individuals to save for emergencies, medical expenses, and long-term goals without jeopardizing federal benefits eligibility. Eligibility for ABLE accounts requires a disability onset before age 26, with options for SSI/SSDI recipients and those with a disability certification.

ABLE accounts enable individuals with disabilities to save money while retaining eligibility for federal benefits programs. These accounts can be used for various expenses, including education, transportation, and healthcare, and offer tax advantages. The ABLE Act also allows for contributions beyond the annual limit for employed individuals and provides opportunities for savings and financial stability.

ABLE accounts, designed to supplement other benefits, can be used to pay for vocational rehabilitation (VR) services, ensuring more individuals with disabilities are eligible. VR programs should consider assisting individuals with ABLE account setup, as they can enhance financial stability and employability. Additionally, ABLE accounts can be utilized to pay for Medicaid Buy-In Program premiums, allowing individuals to maintain Medicaid coverage while increasing their earned income.

ABLE accounts, designed for individuals with disabilities, offer savings opportunities without jeopardizing Medicaid eligibility. These accounts can be used to pay for employment-related expenses, including premiums for Medicaid Buy-In programs, and provide a safety net for unexpected costs. While ABLE accounts may impact SSI and SSDI benefits, work incentives and support services help mitigate these effects.

ABLE accounts can be used by Social Security beneficiaries to maximize employment outcomes and improve financial stability. Recommendations include utilizing ABLE accounts to save for work-related expenses and aligning them with PASS plans for long-term employment support. The Workforce Innovation and Opportunities Act (WIOA) emphasizes financial literacy education for individuals with disabilities, including information about ABLE programs.

The Achieving a Better Life Experience (ABLE) Act allows individuals with disabilities to save for future expenses, including employment-related costs. State and local Workforce Development Boards can collaborate with state ABLE programs to increase awareness and understanding of ABLE accounts, offering financial literacy education and support for setting financial goals. This collaboration can help individuals with disabilities achieve competitive integrated employment outcomes.

State ABLE programs offer training and resources to support employment goals for individuals with disabilities. Partnerships with workforce development systems and banks can provide financial literacy education and help open ABLE accounts.

Things to Know about ABLE

- ABLE Account Purpose: To improve the financial stability of individuals with disabilities by allowing them to save money tax-advantaged.

- Qualified Disability Expenses (QDE): Expenses related to disability, including housing, transportation, support services, and other expenses.

- ABLE Account Benefits: Exclusion of funds from countable assets for means-tested benefits, enabling individuals to save for emergencies, unexpected medical expenses, education, retirement, and other financial goals.

- Tax Treatment of Qualified Distributions: Tax-free for interest and capital gains.

- Tax Treatment of Non-Qualified Distributions: Taxable on earnings portion, and can affect means-tested benefits.

- Purpose of ABLE Accounts: To pay for qualified disability expenses related to health, independence, and quality of life.

- ABLE Account Benefit Exclusion: Funds in ABLE accounts are generally not counted for federal benefits eligibility, except for SSI beneficiaries with over $100,000 in the account.

- SSI Cash Benefit Impact: ABLE account funds exceeding $100,000 for SSI beneficiaries can impact their monthly SSI cash benefit, but not other benefits like Medicaid.

- ABLE Account Contribution Limit: ABLE accounts have a yearly contribution limit of $15,000 per year, allowing individuals to save earned income without jeopardizing government benefits eligibility.

- ABLE Account Contribution Limit: $15,000 per year for individuals with disabilities.

- Impact on Medicaid Eligibility: Contributing to an ABLE account allows individuals to maintain Medicaid eligibility while saving for the future.

- State-Sponsored Programs: ABLE accounts must be opened through state-sponsored programs or the District of Columbia.

- Residency Requirements: Most ABLE programs have no residency requirements, allowing individuals to open accounts regardless of their state of residence.

- Eligible Individual: Individuals with disabilities that began before age 26 and who received SSI or SSDI benefits, or those with a disability certification meeting specific criteria, are eligible for ABLE accounts.

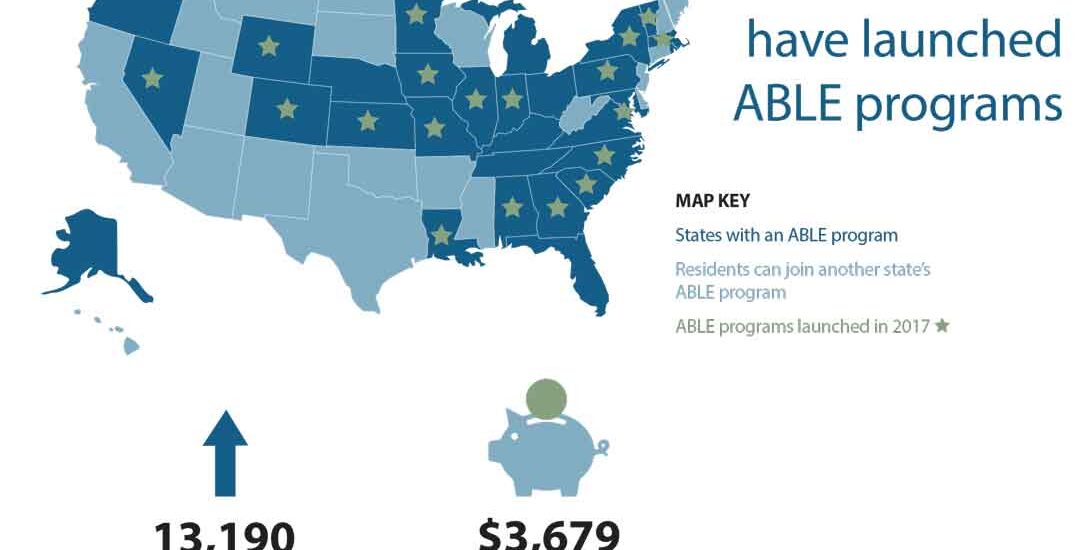

- ABLE Program Availability: As of the writing, 42 states and the District of Columbia offer ABLE programs, with varying eligibility requirements for residency.

- ABLE Account Eligibility: Individuals with disabilities, regardless of work limitations, can apply for an ABLE account, especially those eligible for federal benefits programs.

- Qualified Disability Expenses (QDE): Expenses like education, transportation, personal assistance, healthcare, and housing qualify as QDE, meaning withdrawals from ABLE accounts for these expenses are tax-exempt.

- Impact on SSI Eligibility: ABLE account owners can save up to $100,000 without losing SSI eligibility, exceeding this limit may impact SSI benefits.

- Impact on Other Benefits: ABLE savings do not impact eligibility for other federally funded, means-tested benefits.

- SSI Asset Limit and ABLE Account: ABLE account balance exceeding the SSI asset limit may cause SSI suspension until resources decrease.

- ABLE Account Contribution Limits: ABLE account can hold up to the state’s 529 college savings account limit ($529,000) with a maximum annual contribution of $15,000.

- ABLE Account Contribution Limit: ABLE account owners who work can contribute their earnings or an additional $12,140, whichever is less, into their ABLE accounts.

- Impact of ABLE Accounts on Working Adults with Disabilities: ABLE accounts provide savings options for emergencies and unexpected expenses, which were previously limited for individuals with disabilities.

- Employer-Sponsored Retirement Plan Contribution Restriction: Contributions to ABLE accounts are limited if the individual or their employer has contributed to an employer-sponsored retirement plan (401(a), 403(a), 403(b), or 457(b)) in the same calendar year.

- Financial Security: People with disabilities may face financial insecurity due to unexpected expenses, potentially leading to job loss.

- Savings Limitations: Asset caps in programs like SSI and Medicaid Buy-In often prevent individuals with disabilities from saving for unexpected expenses.

- ABLE Act Benefits: The ABLE Act allows individuals with disabilities to save beyond asset limits, potentially enabling them to save for retirement, housing, college, or long-term healthcare.

- ABLE Account Usage: Can be used for college tuition, housing, medical care, long-term care, and out-of-pocket medical expenses.

- Financial Stability: Provides a buffer for individuals with disabilities in case of interrupted benefits or for covering disability-related expenses.

- Medical Expenses: Helps cover copays and other extra medical expenditures not covered by insurance, promoting consistent access to healthcare.

- VR Service Goal: To help people with disabilities gain and maintain employment.

- VR Service Funding: VR is the primary source of public funding for supported employment and job training services for people with disabilities.

- VR Eligibility: People with disabilities with significant physical or mental impairments are eligible for VR services.

- ABLE Account and Employment: ABLE accounts can be used to support employment outcomes for people with disabilities.

- VR Program and ABLE Account: VR programs should not consider ABLE account funds when determining financial need for program eligibility.

- Exemptions from Financial Needs Testing: People receiving federal needs-based benefits programs, such as SSI or SSDI, are exempt from financial needs testing.

- ABLE Account Funds Exclusion: ABLE account funds should be disregarded when determining a beneficiary’s contribution to VR services.

- Vocational Rehabilitation Services: Authorized by the Rehabilitation Act of 1973, funded by a combination of federal and state funds, and generally provided by individual states.

- Example of ABLE Account Exclusion: Abed, unemployed and out of high school, has $80,000 in savings in an ABLE account. VR counselors should disregard the ABLE account and determine that Abed will not contribute anything to the cost of services.

- ABLE Account Setup Assistance: VR program counselors should provide information and assistance to beneficiaries seeking to set up ABLE accounts.

- Financial Literacy and Independence: Assistance with ABLE account setup can improve beneficiaries’ financial literacy and independence.

- ABLE Account Funding for Employment Services: VR funds and funds in an ABLE account can be used to cover employment services, increasing eligibility for VR.

- Order of Selection: VR agencies prioritize individuals with the most significant employment needs.

- Rehabilitation Act Requirements: States must prioritize individuals with the most significant employment needs and provide services to all beneficiaries to gain and maintain employment.

- Ohio’s Order of Selection: Categorizes individuals into three priority levels: Most Significant Disability, Significant Disability, and Other Eligible Individuals.

- ABLE Account Usage for VR Waiting List: Individuals on VR waiting lists can use ABLE accounts to fund services related to their vocational goals.

- ABLE Account as Financial Security: ABLE accounts can provide financial security for individuals awaiting VR services or when VR benefits are limited.

- ABLE Account for Job Coaching: ABLE accounts can be used to fund additional job coaching services when VR services are exhausted.

- ABLE Act’s Role: Supplements, not replaces, other benefits and services, potentially covering gaps and enabling Medicaid retention.

- ABLE Account Usage: Can be used to pay for Medicaid Buy-In Program premiums, allowing beneficiaries to earn more income.

- ABLE Act and Medicaid-Funded HCBS: Recommendations focus on using ABLE accounts with Medicaid-funded HCBS to improve employment outcomes for people with disabilities.

- Medicaid Buy-in Program Eligibility: Individuals with disabilities earning above Medicaid’s income limits can qualify by meeting specific requirements and paying a premium.

- Medicaid Buy-in Program Requirements: Participants must meet all disability-related SSI requirements except income and asset limits, and pay a state-specific premium.

- Medicaid Buy-in Program Limits: Each state sets its own income and asset limits for the program.

- Medicaid Buy-In Programs: Allow working people with disabilities to maintain Medicaid eligibility and access employment and health insurance supports.

- ABLE Accounts and Medicaid Buy-In Programs: Individuals can use their ABLE accounts to pay premiums for Medicaid Buy-In programs, allowing them to maintain eligibility and build savings.

- Transitioning Between Medicaid Programs: Individuals can transition between Medicaid Buy-In programs and traditional Medicaid based on income, without needing to spend down savings.

- Medicaid Eligibility Criteria: Individuals must meet the SSI definition of disability, have monthly earned income under $3,433, and possess less than $25,000 in non-exempt assets.

- ABLE Account Benefits: ABLE accounts allow individuals with disabilities to save money while maintaining Medicaid eligibility, potentially reducing reliance on income support programs.

- Recommendation for Medicaid Case Managers: Provide assistance in linking individuals to support for setting up ABLE accounts.

- ABLE Account Setup: Jacquan, with the help of a benefits counselor, sets up an ABLE account to pay for expenses not covered by Medicaid.

- ABLE Account Information: Jacquan and the benefits counselor use the website www.ablenrc.org to learn about ABLE accounts and compare different state programs.

- ABLE Account Eligibility: Juan, who is concerned about losing Medicaid eligibility due to saving for a car, is advised to open an ABLE account.

- ABLE Account Usage for Employment Services: ABLE account funds can be used to pay for employment supports in emergency situations or when other funding sources are insufficient.

- Medicaid Eligibility and Savings: Family members’ contributions to ABLE accounts do not impact an individual’s Medicaid eligibility, allowing them to save for a car without jeopardizing services.

- Increased Earned Income with Better Transportation: Improved transportation, such as a car purchased with ABLE account funds, enables individuals to work more hours, leading to increased earned income.

- Medicaid Coverage for Services: Medicaid covers approximately 30 hours per week of job coaching and personal assistant services, as well as transportation.

- ABLE Account Usage: George uses funds from his ABLE account to pay for dry cleaning and to cover unexpected transportation costs.

- Eligibility for ABLE Accounts: Individuals with disabilities receiving SSI or SSDI benefits must have an onset of disability date prior to age 26 to be eligible for an ABLE account.

- Work Incentives Impact: Social Security work rules, applied to earnings, can affect countable income, potentially impacting Social Security benefits and ABLE account deposits.

- SSI Earnings Deduction: SSI beneficiaries lose $1 for every $2 earned after deductions, resulting in a higher total income.

- SSDI Earnings Impact: Earnings after a nine-month trial work period are subject to countable income rules, potentially affecting SSDI cash benefits.

- Safety Net for Beneficiaries: Social Security provides expedited reinstatement of benefits for eligible individuals who lose their benefits due to successful employment and return-to-work efforts.

- Medicaid and Medicare Coverage: Beneficiaries may maintain Medicaid and/or Medicare coverage even after losing Social Security cash benefits through various provisions like EPMC, Medicare Buy-In, and 1619(b).

- Work Incentives: Social Security offers work incentives, including Extended Period of Medicare Coverage (EPMC), Medicare Buy-In, and the purchase of “Medicare for Persons with Disabilities Who Work” after EPMC expires.

- ABLE Account Impact on SSI Benefits: Unearned income deposited into an ABLE account is disregarded, and interest, dividends, or appreciation in value are also disregarded. Up to $100,000 saved in ABLE accounts does not count towards the SSI resource limit.

- SSDI Benefits and ABLE Accounts: ABLE accounts do not impact SSDI cash benefits.

- SSI Eligibility Requirements: SSI cash benefits are means-tested, with resource limits of $2,000 for individuals and $3,000 for eligible couples.

- ABLE Account Funding Sources: Individuals receiving SSI can use monetary gifts and savings to fund their ABLE accounts.

- ABLE Account Spending: ABLE account funds can be used for qualified disability expenses, including some employment-related expenses.

- SSI PASS Program Integration: The SSI PASS program allows SSI recipients to save for work goals while potentially maintaining their SSI benefits.

- ABLE Act and Workforce Development: The ABLE Act, in conjunction with the Workforce Innovation and Opportunities Act (WIOA), emphasizes the inclusion of individuals with disabilities in workforce development programs.

- Financial Literacy for Employment: WIOA mandates financial literacy education for job seekers with disabilities, including information about ABLE programs, to support their employment goals.

- Financial Literacy Program Elements: Financial literacy education under WIOA encompasses nine program elements, including budgeting, saving, managing spending, credit, and debt.

- Financial Literacy Education: Teach about credit reports, scores, rights, inaccuracies, and improving credit.

- Financial Product Understanding: Support understanding, evaluation, and comparison of financial products and services.

- Identity Theft Protection: Educate about identity theft, prevention, and resolution, including rights and protections.

- ABLE Account Promotion: State and local Workforce Development Boards can promote ABLE accounts for individuals with disabilities to support career pathways and skills development.

- Partnership with ABLE Programs: Boards can collaborate with state ABLE programs to improve recruitment of eligible individuals and provide financial goal setting support.

- Financial Literacy Education: Boards can offer financial literacy education, such as classes on setting financial goals and opening ABLE accounts, to individuals with disabilities.

- Financial Literacy Education: American Job Centers, in collaboration with state ABLE programs and banks, should offer financial literacy education to job seekers.

- ABLE Account Benefits: Financial literacy education should include information about the benefits of ABLE accounts for obtaining or retaining employment.

- Example of ABLE Account Use: Mary, a job seeker, uses an ABLE account to save for a computer, internet access, and transportation.

- ABLE Account Benefits: Tax-advantaged disability savings accounts for future expenses, including emergencies, community living, healthcare, benefits planning, and financial counseling.

- Eligibility Expansion: The “ABLE Age Adjustment Act” increased the age of eligibility to open an ABLE account to 46 years old.

- Recommended Usage: Vocational rehabilitation staff can assist beneficiaries in signing up for ABLE accounts and using funds for financial stability or work-related expenses. Medicaid beneficiaries can use ABLE accounts to pay for Medicaid Buy-In Program premiums or employment-related services.

- ABLE Account Promotion: Staff in Medicaid programs should connect beneficiaries with organizations and individuals who can assist them in setting up ABLE accounts.

- Benefits Counseling Importance: People receiving public benefits should seek out benefits counseling and financial planning to make informed choices about their options.

- Financial Literacy Education: Youth and adults with disabilities should seek financial literacy education programs and services to understand and make informed decisions about financial products and opportunities.

- ABLE Act Objective: To maximize competitive integrated employment outcomes for individuals with disabilities.

- Vocational Rehabilitation System Collaboration: State VR agencies partner with state ABLE programs to educate VR counselors and clients about ABLE account benefits for employment goals.

- Medicaid System Partnership: State Medicaid agencies collaborate with other agencies to promote ABLE account awareness, understanding, and utilization for employment support.

- Public Funding Source: State Medicaid agency can help identify ABLE-eligible individuals and provide information about ABLE accounts.

- Social Security Beneficiaries Support: Social Security Community Work Incentive Coordinators receive information and training to support employment goals of ABLE-eligible beneficiaries.

- Workforce Development System Partnership: State and local Workforce Development Boards can partner with state ABLE programs and banks to offer financial literacy education and support employment goals.